“Can I afford to send my child to university?” It is a question many parents have in mind. Although the answer is hopefully a “yes”, you will have to plan ahead. Unless you are financially very well off, you cannot expect to do nothing for years, and then magically find the fund to pay for your child’s tertiary education expenses. The best thing to do is to start saving as early as possible, even if you’re able to save only a small amount at the beginning.

If you would like to skip this article and go straight to find out how much tertiary education for your child will cost in the future, go to this page to complete the survey to get your FREE Education Fund Report.

What expenses are included in the annual cost of tertiary education?

In general, the annual cost of tertiary education consists of Tuition Fees and Room & Board. However, to be more precise, there are five categories of expenses to determine the total cost of attending a university/college:

- Tuition and fees: This amount is depending on the field of study (In some countries, international students pay higher than the local students)

- Books and supplies: Varies base on the field of study and course requirements, students can buy used books to save cost.

- Room and Board: Varies base on meal plan selection (for on-campus students). Usually living off-campus is cheaper than living on-campus and students can opt to cook their own meals to save cost if they are staying off-campus.

- Transportation: Depending on where a student lives in relation to the school. Overseas students may incur additional expenses to visit home countries.

- Personal expenses: The amount varies depending on lifestyle. (e.g. Health insurance, telephone bills, entertainment)

The latter three categories depend on personal lifestyle. Thus, your child actual expenses may be less than or more than the estimated average cost you would find from the respective universities’ websites.

How much will tertiary education cost in the future?

The key word here is “future”. Once you have decided where you would like your child to receive his/her tertiary education, you can research for the average cost in today’s value. However, since your child is not going to university now, the cost to attend a university in the future is going to be more than now. This is due to inflation in living expenses and tuition fees. For example, the average cost (tuition fees and living expenses) for a four-year private college in Malaysia is RM112,000 (source: Public Mutual University Cost Guide 2013). This amount will become RM319,686 after 18 years if the inflation rate is 6.0% p.a. Thus, when calculating the future tertiary education cost, you must include the inflation in your projection.

How much should I save?

Basically, you will want to put aside as much money as possible in your child education fund. The more money you put aside now, the lesser you or your child will need to borrow later. Start by estimating the education cost for a 4-year study at a university of your choice. Then, you decide how much of the bill you want to fund, i.e. 100%, 75%, 50%, and so on. With the future amount of education fund being estimated, you have established a financial goal.

Depending on your own risk profile, you may put aside regular savings into investment portfolio that potentially yield high return or put aside regular savings into Fixed Deposit that yield low return (risk-free return). Alternatively, you can choose a moderate return with moderate risk investment portfolio. The same amount of money put aside regularly into different investment portfolio will yield different amount of fund at the end of the day. Chart 1 shows projected education funds that can be accumulated for conservative (3% p.a.), moderate (6%) and moderately aggressive (8% p.a.) portfolios at the end of 18 years. Lower return will reduce the education fund available in the future. To compensate for the shortfalls, you will have to put aside more money if you choose a lower return investment tool. Ideally, you want to put aside an amount of money that is affordable, regularly, into an investment tool that matches your investment risk profile. The invested amount must be able to create an education fund that is equal to or more than the amount that your child will need when he/she reaches the age of tertiary education.

In reality, the amount of money you can contribute depends on how much you can afford to contribute. There are too many competing financial needs for you and your family, such as retirement planning, buying a new house, changing a new car, vacations, and etc. If you find that you cannot afford to contribute as much as you plan to, you will need to take a detailed look at your family’s finances in order to determine what expenses are optional, and re-prioritize other competing financial goals. Ask yourself questions like: “Do I need to change car?”, “Can I just have one car instead of two?”, “Can I eat out less?”, “Do I want to spend my unanticipated windfalls like bonuses, or pay raises on a new 60’ LED TV or an iPhone 8?”

Start a saving program as early as possible

Perhaps the most difficult time to start an education fund saving program is when your child is young. New parents face a lot of financial strains such as the possible loss of one income, child-related spending, and the competing needs to save for a house or car. However, this is the time when you should start saving.

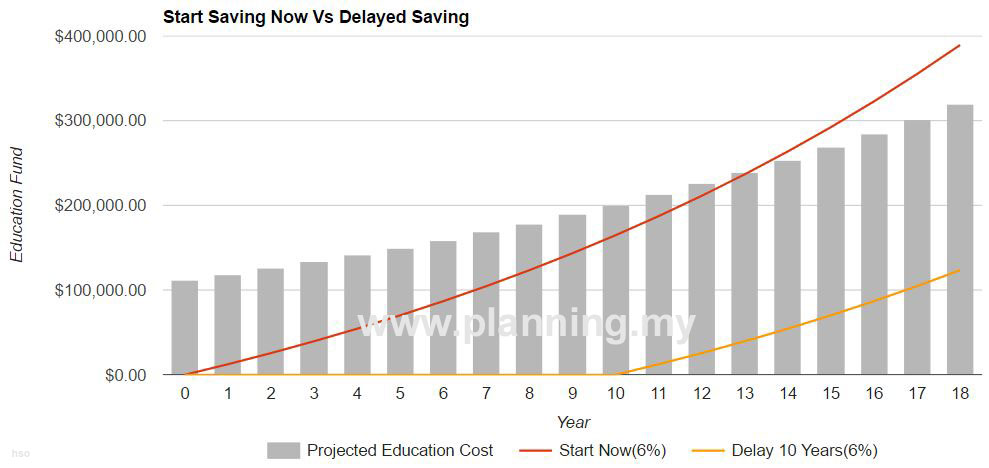

When you start early, you have many years to go until your child starts his/her tertiary education. Thus, you have the option to select an investment that has the potential to outpace education cost inflation, i.e. investment return that can outpace the tuition fees inflation. Another benefit of starting early is compounding effect of your money. It means the return of your investment in the past will be able to earn interest/return in the future. When you start early, your money can compound for longer time before you need it. The following chart shows how early start can make a big difference in the future. It does not matter if you cannot afford the amount that you suppose to put aside now. You can put aside as low as $100 per month and later increase the amount when you can afford it. This is better than doing nothing now because delaying will only cost you more in the future.

How can I fund the education fund?

This is also one important question parents always have. Should I put aside the money in unit trust investment, bank savings, stock market, property investment or in an education insurance plan? There is no one answer for everyone. In fact, usually parents will need a hybrid solution. This is a balancing act of risk, investment return, and investment horizon.

- Risk: We can plan everything, but we must understand that we made a couple of assumptions during the planning. We assume inflation rate unchanged. We pick the average college expenses that may be more than or less than the actual cost. We also assume that the source of funding will not be interrupted, and there is no currency fluctuation.

- Investment Return: It is not a guaranteed return. Although we can manage the investment portfolio risk, the actual investment return always depends on the market conditions that are out of our control. Higher return usually comes with higher risks, and lower return usually is associated with relatively lower risks.

- Investment Horizon: If you start early, your investment horizon is longer. Hence, you can have more options with the same amount of budget. You may choose a lower risk investment tool, and still be able to achieve your goal. Alternatively, you can take higher risk since you do not need the fund in the short term. However, if you start late, the remaining time before your child go to university/college is shorter. With the same budget, your only hope is to put your money to work harder for you. However, that also means you need to take a higher investment risk. In fact, when your investment horizon is short, you should put in more money rather than taking higher investment risk. This is because you will need the money in a few more years. You want to make sure that the money will be there when you need it and not subject to investment lost due to high investment risk.

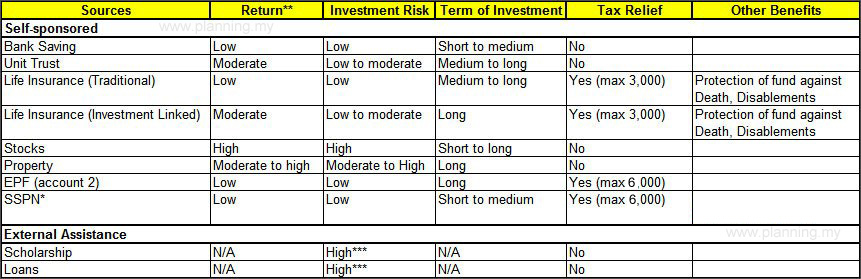

The following table shows various investment options and the respective risk, return, and investment horizon. It is also good to know that education insurance allows you some tax relief. This tax saving may enhance your return if you put the tax saving back into the education fund. (The tax relief, SSPN, and EPF is only applicable in Malaysia, please ignore them if you are not from Malaysia)

[Update: For latest education cost, please refer to Public Mutual University Cost Guide 2017 (9th Edition)]

* Skim Simpanan Pendidikan Nasional

** Low means annual return less than 4%, moderate 4%-8% and high above 8%

*** No guarantee of getting

If you would like to find out how much tertiary education for your child will cost in the future, go to this page to complete the survey to get your FREE Education Fund Report.